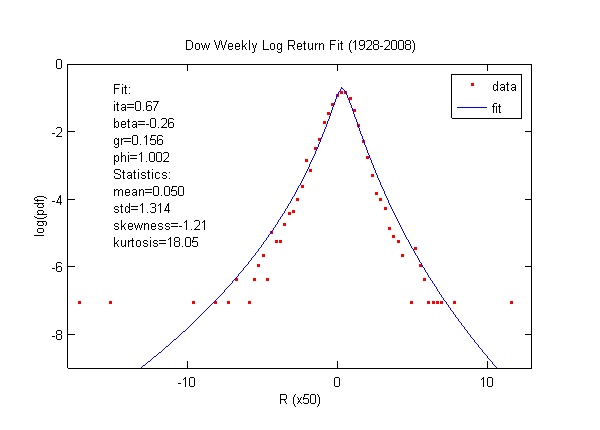

The Dow weekly log return has a smaller kurtosis than the daily log return.

However, the kurtosis is still very significant.

The general shape of the distribution fits the skew lognormal cascade distribution well.

But the fit has to choose between kurtosis and variance. They can not be matched exactly at the same time.

The fit presented here weights more on getting to the kurtosis.

And the tradeoff is that the variance of the fitted curve is slightly bigger.

Data Source: Yahoo Finance