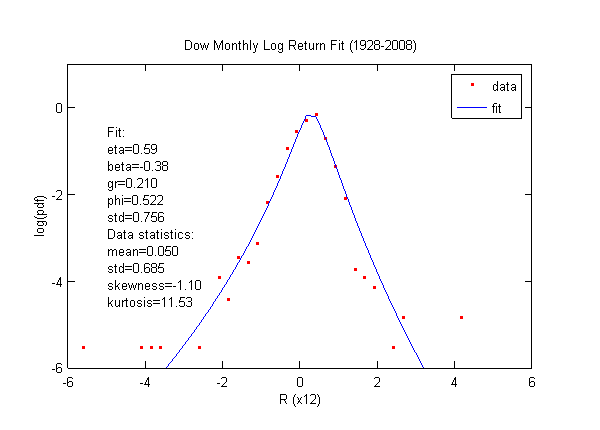

The Dow monthly log return has a much smaller kurtosis (~11) than the daily log return.

However, the kurtosis is still very significant.

The general shape of the distribution fits the skew lognormal cascade distribution well.

This indicates the cascade kernel of the monthly log returns is normal (unlike the daily distribution).

Data Source: Yahoo Finance